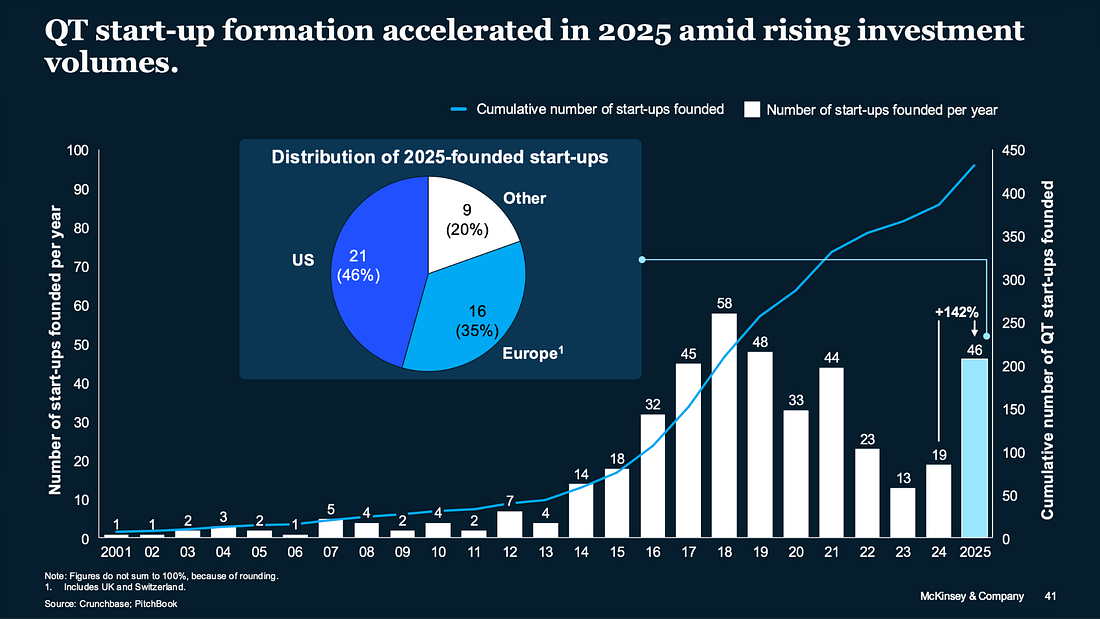

Hi there, One last read before you trade the office for beaches and out-of-office replies: the 139th edition of Heartcore Insights, curated with 🖤 by the Heartcore team. If you missed the past newsletters, you can catch up here. Now, let’s dive in! Market CommentaryThe last months haven’t been great for Team “Application Layer.” We’ve been questioned around the moats, how frontier labs are eating into our lunch, and products kept being dismissed as “UI on top of database”. Frontier labs are closing mega-rounds while more than two hundred once-funded unicorns have quietly fallen. The best anecdote to illustrate this state of mind is Bain Capital revealing they have a dedicated team vibe coding replicas of targets to stress test their defensibility. Deals would be killed based on the results. My view: the confusion comes from the fact that we’re still using the old definition to evaluate the new thing. The old one is what Bain is replicating: a UI, a database, a sales team. You would build an application, sell seats, expand modules, and grow with headcount. Of course, this approach is under pressure. However, the new model is breaking the old apart and being rebuilt around new sources of value. This definition has three load-bearing parts: A Model-Agnostic HarnessFable 5 was pulled globally in 72 hours by the US government. Single-model dependency is now an existential risk. When a single government decision can zero out your product overnight, model-agnosticism stops being an architectural preference and becomes table stakes. The other part of this story is that Fable opened a 5 point lead on Arena leaderboard and GLM-5.2 halved it within a week (!) with an open weights model. A lead that lasts a week is the opposite of the durable, compounding edge that would suck all application value into the research labs. This is what Cursor and Fin (previously Intercom) understood. Neither locked to a single model provider. Fin routed across open-source and commercial models depending on cost and task complexity. Cursor lets users pick between Claude, GPT, and others. The harness isn’t just a technical choice, it’s the foundation everything else sits on. A Data Loop that Compounds into Model BehaviourBoth built compounding loops where usage improved the product automatically. Yes, this is something that also happened pre AI. However, in the pre AI phase, more usage improved the inputs to a static system, and the improvement was episodic. Today, data improves the system itself, and it’s continuous. Also your software doesn’t get better at routing and ranking (think Spotify knowing I like bossa nova) but at making the right judgment. Fin’s model got better at knowing when a customer was about to churn before the customer said it. This is accumulated judgment. And when a company has enough usage, proprietary dataset, and economic incentive, they will pull intelligence in house. Cursor introduced Composer 2, training a 1.5 trillion parameter model from scratch using the coding traces of 5 million developers. Intercom made a similar move and introduced Fin Apex, their own vertical model trained on 40 million support conversations. This is the age of vertical models, and it only becomes available to companies that run the loop long enough. No one can vibe code that, not even Bain ;) Outcome-based CommercialisationEnterprises are waking up to an AI hangover, after a night out token maxing without knowing the ROI. Finance has no mental model for a cost that fluctuates by task, model, and token count. Uber blew up its entire AI budget in four months, and other clickbait stories made the rounds. All the way to our COO’s desk (hi Signe!). She now asked us to run some financial analysis in respect to our AI consumption. No one is escaping the consumption audit phase this summer (fun times). Both Cursor and Fin priced on outcomes rather than seats. The customer pays for what the product did (a closed ticket, a shipped feature) not for access to the tool. I’ve been investing for five years, and never have I seen a more intense rate of pricing testing within companies today. Historically, companies were too scared of changing their pricing model with the fear of losing well earned revenue, but the rate of product development and competition has led pricing to shift from a one off change to a continuous reflection. Which is what makes Cursor’s official $60B exit to SpaceX and Fin’s acquisition by Salesforce so instructive. What matters is how they architected (the harness), and what they optimised for (intelligence per dollar). The latter will go down in the history book as one of the most impressive come back stories in company building. Reminder: the company had 7 consecutive quarters of zero net new growth which led the founder to come back in full founder mode and re-adapt the company to the age of AI. The definition of an application company is being rewritten. The old one: a UI, a database, a sales team. One version of the new one: a harness, a compounding loop, and eventually a model no one else can train. But there is a second version growing just as fast, maybe faster. Companies that looked at the same opportunity and decided the real leverage wasn’t owning the intelligence (the layer down), but owning the outcome (the layer up). Instead of selling the tool, you sell the end results. When AI is capable of delivering the last mile, the software company doesn’t just build better software. It becomes a service. More about that next month. ~Naza Metghalchi, Partner, Heartcore Capital The Roadmaps are Converging on 20282024 was the year of quantum computing roadmaps, when vendors started to trade vague promises of advantage for specific, dated targets. Two years on, the discipline has hardened: with Heartcore’s QC Roadmap tracker we identified nineteen vendors with committed, processor-named roadmaps, and the unit of competition has moved from physical to logical qubits. As the targets sharpened, they clustered: sixteen of the nineteen now aim at the 2027 to 2030 window for early utility machines. And rather than slip those dates to buy time, several teams are pulling them forward. Last week, that private consensus became public policy in the US. On Monday, President Trump signed an executive order launching a national effort to build the first quantum computer powerful enough for scientific discovery and place it at a Department of Energy facility by 2028, a timeline the White House calls achievable, and the next day the Department of Energy answered with Quantum Genesis, its program to deliver that machine. QuEra, unveiling its own roadmap the same week, put Libra on AWS in 2028 and charted a path beyond 1,000 logical qubits by decade’s end. A Second Wave of BuildersBut a roadmap is only a promise. Delivering one takes innovation that does not yet exist, and a second wave of founders is now supplying it. The first wave of quantum startups, from roughly 2014 to 2023, proved the physics. The second, from 2024, is tackling engineering: the heat and wiring of superconducting qubits, the laser delivery for neutral-atom arrays, the coupling efficiency of qubit-photon interfaces. None is solved, but each is now quantified, and that is the point. A scaling problem that is finally well-posed is a company waiting to start, and founders are coming straight out of the universities and labs to start it. The data shows it: McKinsey counts 46 new quantum startups founded in 2025, a 142% jump over 2024 and closing on first-wave peaks (Figure 1). And these recent numbers are understated. I can reassure you of that, having spoken with more early-stage startups than those reports capture.

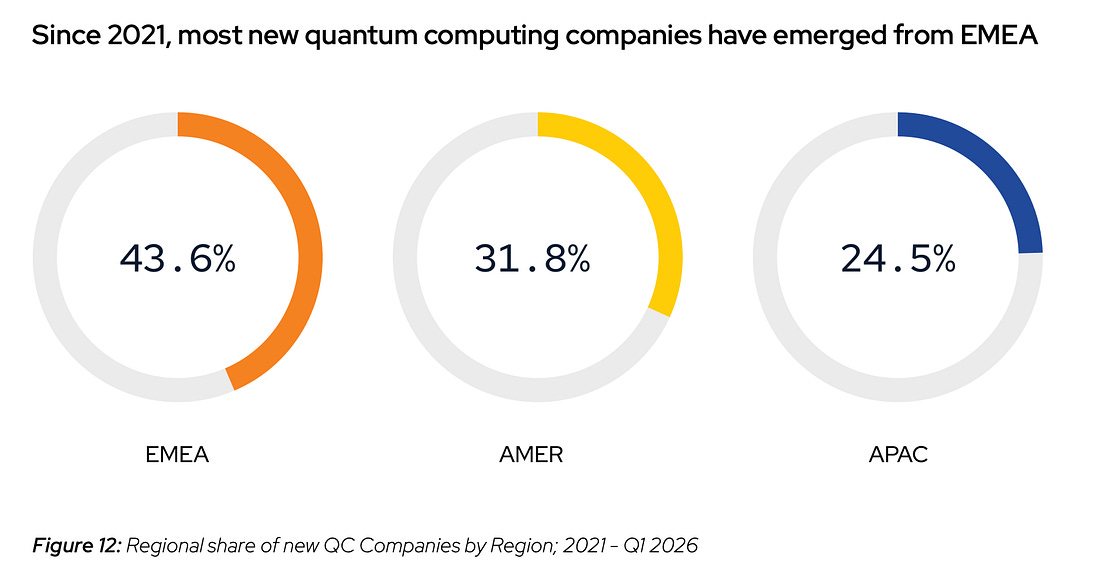

Europe’s StrengthAnd a striking share of those builders are European. The US may have led new formation in 2025, but since 2021 EMEA has produced 43.6% of all new quantum companies (Figure 2), more than the Americas (31.8%) or APAC (24.5%). The foundation underneath that number is talent: the QED-C’s State of the Global Quantum Industry 2026 report finds the EU leads the world in pure-play quantum workers with 6,420, ahead of the United States at 4,401. Europe has seen this and is building on it, through continent-scale infrastructure and a pipeline of physicists and engineers few regions can match. The result is a steady stream of companies turning research depth into products. From where we sit, this is the most encouraging signal in the sector, larger than any single breakthrough: a deep and widening base of people choosing to build here.

Keep it coming. If you are starting something in quantum hardware, enabling infrastructure, or the software stack that ties it together, we would love to hear what you are working on. ~Michael Baczyk, Investor, Heartcore Capital

🖤 Heartcore News

Thank you for being a loyal subscriber of our monthly Insights. Please feel free to share this newsletter with anyone you’d think would appreciate it!

|

Thursday, July 2, 2026

🍦 Heartcore Insights

Subscribe to:

Post Comments (Atom)

Weekly Growth: AI Paywalls, Smarter Advertising & the Return of Claude Fable 5⚡️

Short. Smart. Addictive. ...

-

On Monday, Leon County Circuit Judge Angela Dempsey rejected Bear Warriors United's request for a temporary injunction to halt the s...

-

Police say information from a Reddit tipster who had a strange encounter with another man on a sidewalk outside Brown University provi...

-

The Trump administration has launched a new federal initiative called the U.S. Tech Force, aimed at hiring about 1,000 engineers and t...

No comments:

Post a Comment