That’s the share of American adults who identify as gay or lesbian, down from 4.7% in 2020.

Bulls vs. bears: Who’s right about this market?

SpaceX survived its lockup. Its Q2 earnings? Not so much

Last week, the S&P 500 hit fresh record highs … twice. On Tuesday, the index climbed nearly 2% to its first record close since June, and the following day it notched another intraday all-time high. So far this year, the index is up 13%, above its long-term average return of 10%.

The rally has led some investors to believe the worst of the AI-driven sell-off is behind us. But not everyone is convinced. Michael Burry recently warned that “it is possible we are near a major top,” adding that the market could be setting up for “a 1987-type fall.”

So who’s right: the bulls or the bears?

The bull case

The bull case hinges on three main arguments. First, Iran and Oman are nearing a deal to manage the Strait of Hormuz, which could be a step toward reopening it to commercial traffic. That would bring down the cost of oil and other goods, lessening the persistent threat of inflation.

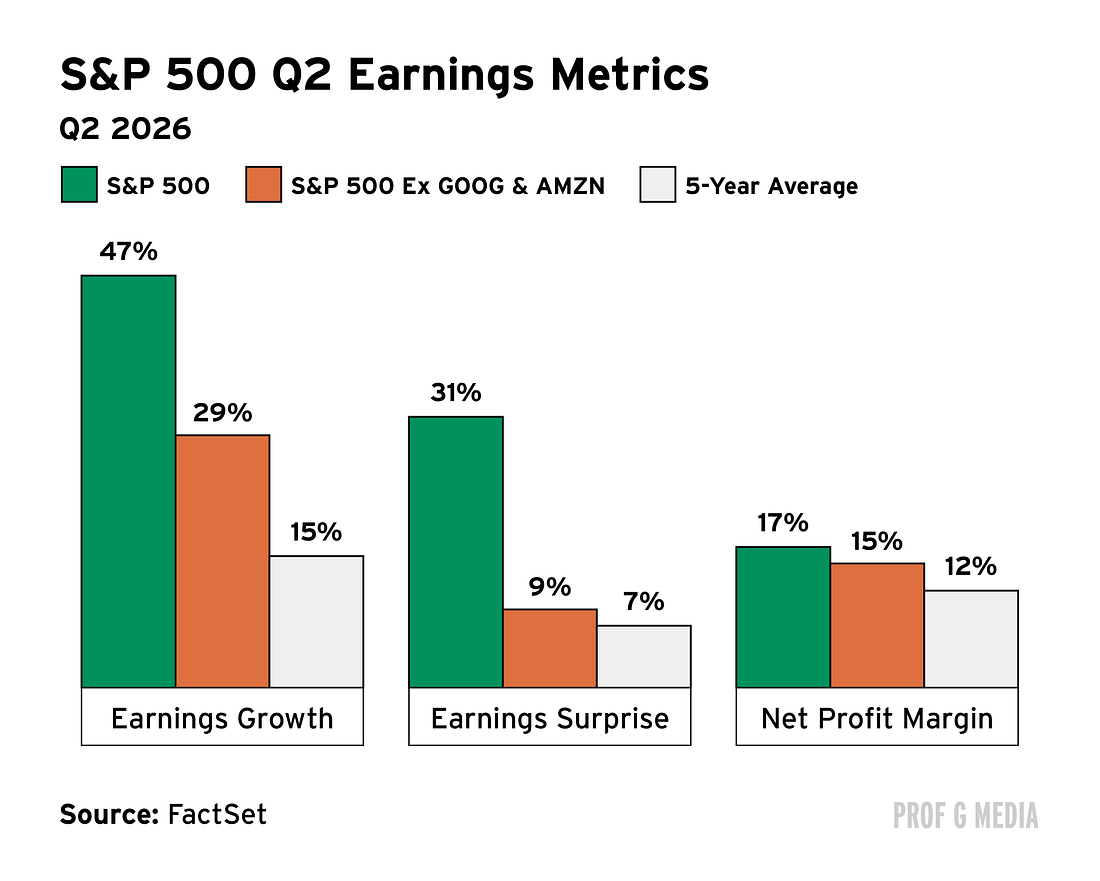

Additionally, second quarter earnings have been strong. The S&P 500 is on track to deliver 27% earnings growth in the second quarter compared with last year — and that’s excluding Amazon’s and Alphabet’s nonoperating, unrealized gains in their equity stakes in SpaceX and Anthropic. That’s more than double the S&P 500’s 10-year average earnings growth of 11%.

The big cloud companies had a particularly strong quarter. Average revenue growth for Microsoft Azure, Google Cloud, and Amazon Web Services (AWS) accelerated from 29% last year to 54% this year.

Josh Brown, co-founder and CEO of Ritholtz Wealth Management, pointed to another bullish signal: “A healthy market takes out its own trash.” Brown isn’t referencing the chore, but rather the recent blowups of particularly speculative trading strategies. Overleveraged investors in South Korea suffered massive volatility and drawdowns, and Leopold Aschenbrenner’s hedge fund was margin-called, as Brown put it, “into the Stone Age.” The rationale is that a healthy, balanced market eliminates overly speculative bets and rewards companies with strong fundamentals.

The bear case

There’s plenty to be nervous about. The most obvious risk is that one unproven bet, AI, is supporting both the U.S. stock market and the economy. Goldman Sachs estimates that AI investment will drive nearly half of S&P 500 earnings growth this year, and Michael Pearce, an economist at Oxford Economics, estimates that AI is responsible for one-third of recent U.S. economic growth.

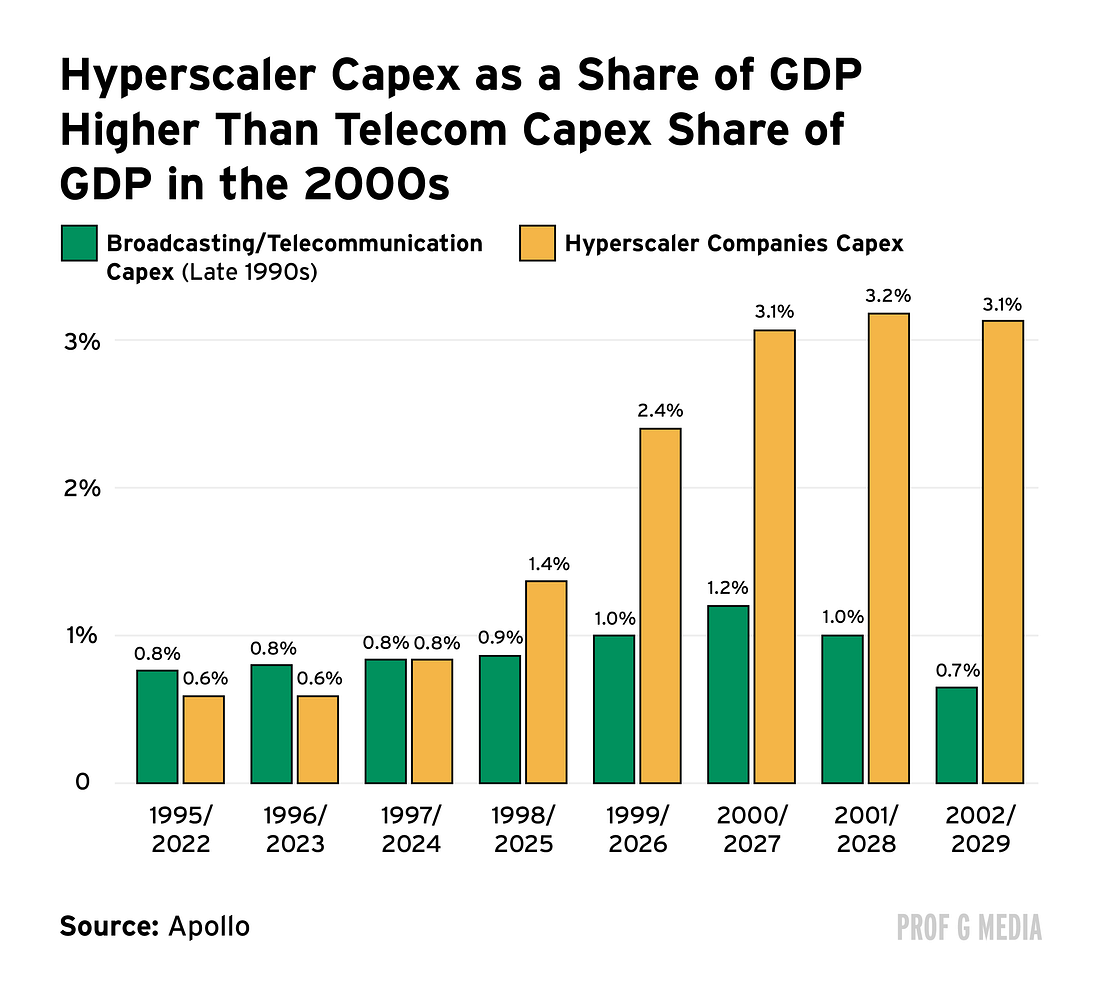

As a share of GDP, capex spending on data centers is now larger than telecom’s share of GDP in the 2000s. It’s also growing faster. AI capex added 0.85 percentage points to GDP in just one year; the housing boom added 0.5 percentage points at its peak, and the telecom build-out added 0.15 percentage points.

This presents a risk. AI has become a crucial source of growth in a short amount of time. If the build-out were to falter, economic expansion would suffer immediately. The sharp reversal would outpace the economy’s capacity to reallocate labor and capital elsewhere.

As Torsten Slok, chief economist at Apollo, explained: “A cycle that builds at 0.85 percentage points a year can unwind at a similar pace, and that, rather than the build-out itself, is the macro risk if AI demand disappoints.”

Capital is flowing to the hyperscalers and neoclouds for their cloud products and data centers; to the semiconductor and memory stocks for their chips; and to materials and industrial companies for their construction of data centers. That’s a diverse array of recipients. But the source of that capital is not diverse. It’s coming from OpenAI and Anthropic. Bloomberg reported last week that OpenAI made up 70% of Microsoft’s AI sales last year, and Ed Zitron has reported the same is true for Amazon and Alphabet.

OpenAI and Anthropic are selling products with unproven ROI, and both are burning tens of billions of dollars a year. If either runs into trouble raising money, the spending stops. And if the spending stops, it’s hard to see how the rest of the build-out doesn’t come down with it.

AI is going to create a lot of winners, but just like the railroads, it’s also going to bankrupt a bunch of people along the way.

If we do have a correction, that doesn’t mean the technology failed. Those are two different metrics, and I think people conflate them. A stock price reflects what investors paid for future growth. A technology’s value is reflected in increased productivity and innovation.

Even if there is a drawdown, America’s risk-aggressive culture has real societal benefits. We make extraordinary investments, we register extraordinary returns, and we accept the accompanying volatility.

Last week marked SpaceX’s first post-IPO lockup expiration, giving employees and early investors their first opportunity to sell shares since the company went public. In total, more than 911 million insider shares became eligible to trade, more than doubling the free float. On the day the lockup expired, the stock increased 6%.

That came just days after SpaceX reported its first earnings as a public company. On the surface, the results looked impressive: Revenue surged 92% year over year, and operating losses narrowed to $143 million from $970 million in the year-ago quarter. The reason for that narrowing? SpaceX added $1.8 billion in new revenue from AI. More on that later.

The majority of SpaceX’s revenue came from Starlink. Sales this quarter increased 66% year-over-year while operating margins increased nearly 3%, and subscribers doubled to 12 million.

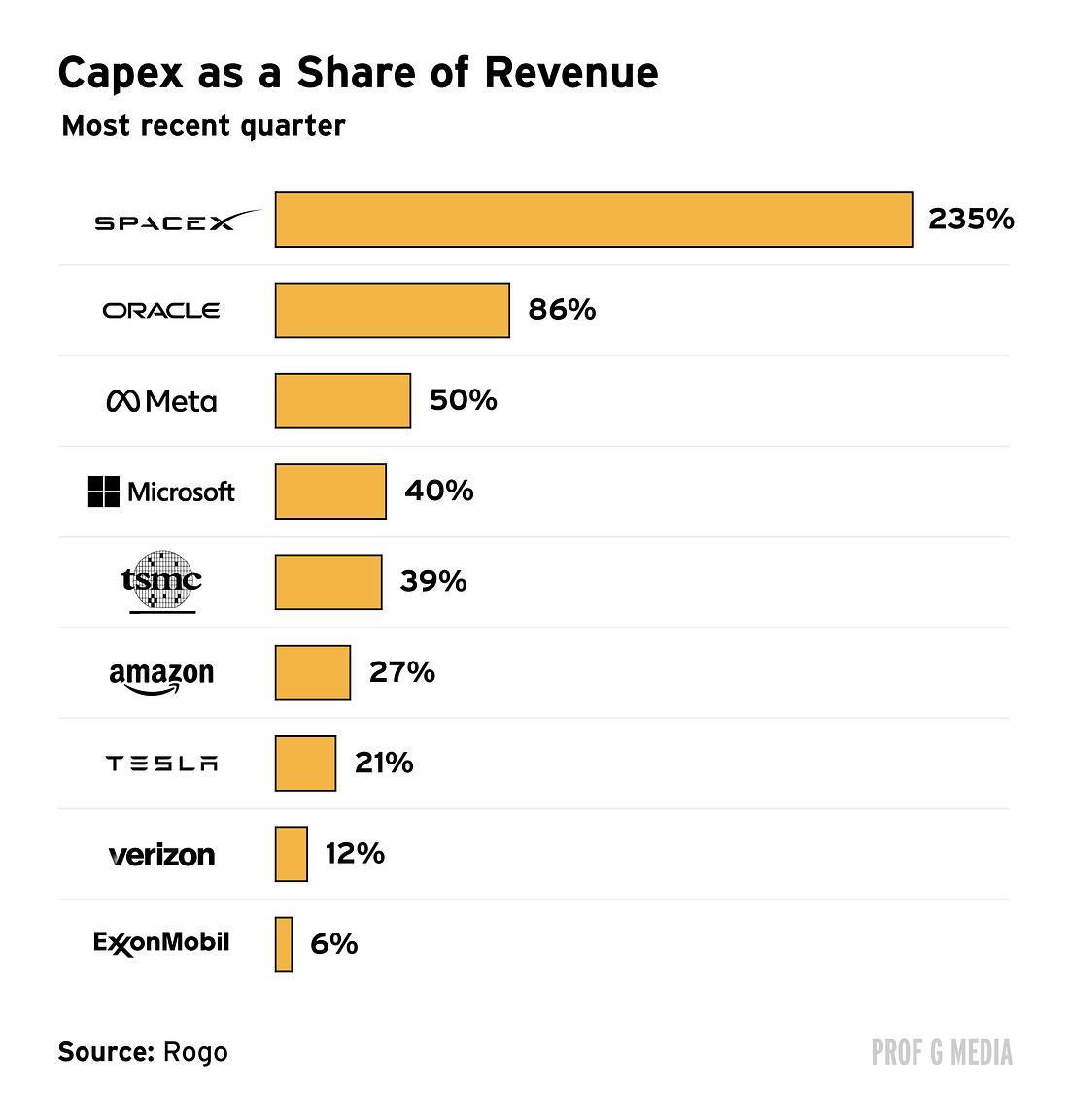

However, the stock fell 14% after reporting earnings because of SpaceX’s skyrocketing capital expenditures, which rose to $18.4 billion this quarter from $2.8 billion last year. At this pace, SpaceX will burn through all $86 billion of IPO proceeds in about 14 months — and that assumes the spend stops accelerating, which it hasn’t.

On the earnings call, CEO Elon Musk told investors that SpaceX will build data centers on the moon “faster than you think,” and that those data centers would be staffed by humanoid robots. In the near term, that seems unlikely. Of the 50 Earthly companies that are working in the field of humanoid robotics, fewer than 10 have advanced beyond small-scale testing. Read more on the gap between humanoid robot hype and reality here.

Overall, SpaceX’s earnings weren’t strong enough to reverse the stock’s decline. SpaceX is down 11% since its IPO and 40% from its all-time high. Musk’s other public company Tesla is also in the red, down almost 30% year to date.

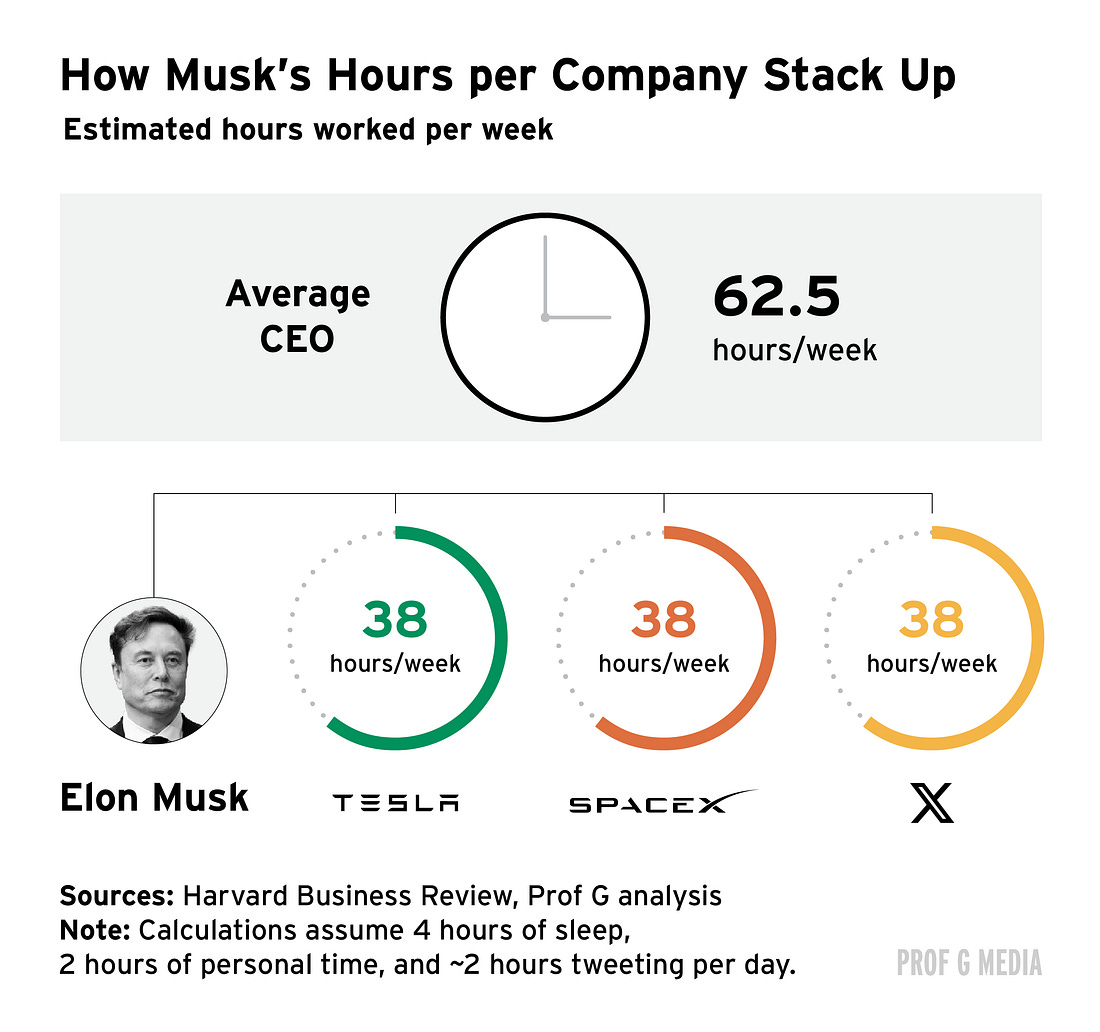

Could the Musk premium be disappearing? It’s hard to imagine how one person could manage being CEO of two public companies and de facto head of a major social media platform at the same time. The mathematical reality is that Musk is a part-time CEO. The question, then, is how long will investors tolerate this arrangement?

My son told me a stat that I thought was so interesting. He said that no one is ever able to stay airborne for longer than a second. Even Michael Jordan. They can get to 0.97, maybe even 0.98, but gravity always wins.

I believe that gravity exists in the stock market, too. Over time, every meme stock just becomes a stock.

It’s happening now to Tesla. Tesla is a great car company, and it should trade at the top of the valuation range for the auto sector, which means it has another 70% or 80% to fall.

SpaceX is an amazing space launch and satellite business that has a near monopoly. But even if it doubles, which it eventually will, there’s still no way to justify the current valuation. In the end, gravity is undefeated.

Elon is spending half his time on Twitter, tweeting about wokeness or about things happening in Minnesota or God knows what.

He has genuinely rotted. He’s totally lost his marbles, and I think we’re finally reaching a point where investors are at least beginning to recognize that. Musk doesn’t sound like some crazy genius who understands things about the future — he sounds like a crazy person who’s lost his grip on reality.

SpaceX’s decline is just beginning, and it will be the tide that drags down all boats.

Aswath Damodaran joins Ed Elson and Scott Galloway to unpack the AI race, his growing concern about the Magnificent Seven, and whether SpaceX’s valuation holds up. Watch here.

What Do You Think Is Acceptable to Wear at the Office? Take The WSJ’s Quiz

Yes, You Can End a Sentence With a Proposition

Want to Run the N.Y.C. Marathon? You May Have to Enter Another Lottery