| | | Healthcare snapshots: Private investment opportunities in healthcare investing are often unique by region, based on differences in population, policy, and public-support sector. Our new reports dive deeper into the trends in EMEA and APAC.

Q2 comp sheets: The first few of our quarterly guides on public company valuations and financials are now available for enterprise SaaS, healthcare services, and medtech

Bioprinting brief: Bioprinting is rapidly moving from science fiction to scientific reality as it reshapes what's possible in healthcare. This emerging field is drawing surging interest from investors, with nearly $335 million raised in the past year alone. Our emerging space brief explores how startups and major players are catching the trend | | | | | | | | | A message from Cherry Bekaert | | | | Cherry Bekaert bolsters fund practice with Spicer Jeffries LLP acquisition | | Spicer Jeffries LLP, a leading CPA firm and top 10 hedge fund auditor, was recently acquired by Cherry Bekaert (the Firm). This strategic acquisition expands the Firm's offerings to clients in the securities industry by leveraging Spicer Jeffries' deep industry knowledge and over three decades of experience. With a combined team of over 500 professionals serving more than 3,600 funds and 3,500 portfolio companies, the Firm's fund clients will have access to unparalleled experience, credentials and resources to achieve their most important business objectives, regardless of size or maturity.

When paired with Cherry Bekaert's audit, tax and advisory services, Spicer Jeffries' securities industry experience and reputation reinforces Cherry Bekaert's standing as a trusted advisor in the financial services sector.

Read more | | | | | | | | | AI in fintech: When term sheets mirror Silicon Valley billboards | |  | | Early-stage fintech valuations: AI vs. non-AI | | | They say a picture is worth a thousand words.

But a billboard in San Francisco? Just two: artificial intelligence.

In Silicon Valley circa 2025, every ad insists the company is "supercharged" by AI, or "cutting edge," because their headcount now includes chatbots.

And beyond billboards—on websites, in social media posts, and across pitch decks—companies are quickly slapping "AI-enabled" on anything they offer.

Which raises the question, who is actually AI-enabled?

That's exactly what we set out to uncover this past quarter, starting with one of the industries where AI adoption is moving fast: fintech.

In our emerging tech research note, we've looked beyond high-level marketing noise to identify genuine AI adopters across the US fintech landscape.

We then compared the data for those AI-enabled fintech companies against non-AI peers to find out if AI is truly having an impact on the fintech deal environment.

Here are five of our key findings to show that it is:

1. Nearly a third of US fintech companies now use AI.

2. 80% of those AI-enabled fintech companies are B2B.

3. Almost half of US fintech deals in 2025 are AI-driven.

4. AI-enabled fintech companies see checks that are 8% larger than non-AI peers.

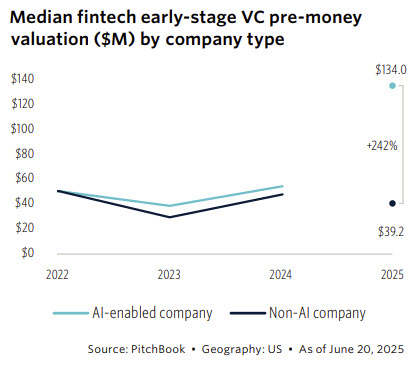

5. Early-stage AI fintech companies currently command a 242% valuation premium.

Putting emphasis on that last point, investors clearly value AI companies with real momentum. And if this trend holds, it's likely that term sheets will soon involve AI as much as billboards do.

The complete picture, including segment-by-segment breakdowns, exit analysis, and our full methodology, is available in our 40-page research note.

Access it here: Fintech's AI Premium

| | Best,

Rudy Yang

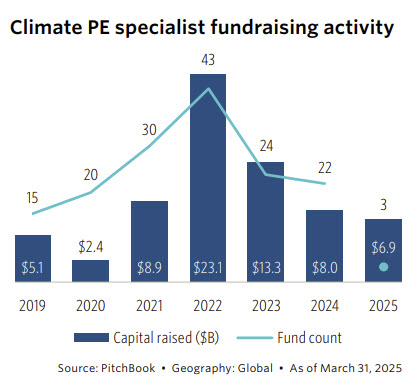

Senior Analyst, Emerging Technology | | | | | | | The growing universe of climate PE specialist funds | | The world of private equity funds that target climate-related investments is continuing to expand, despite the politicization of sustainable investing and other market headwinds. From 2009 through Q1 2025, 260 specialist funds raised $80 billion in aggregate, $63 billion of which was raised from 2020 onward. These funds have become more popular over the past five years as fund managers have increasingly seen the value in developing more concentrated expertise in the space, given its expansion and growing technological sophistication, combined with increased allocator interest.  | | | Fundraising hits its zenith in 2022 with $23 billion raised, and while subsequent years have seen much lower fund counts and raised capital figures, they remain far above averages from 2009 to 2017. Given the smaller sample size of specialist funds, there is some lumpiness in the data, but specialist funds started 2025 with a boom, raising $6.9 billion in only three months. This comes at a time when many are questioning how durable GP and LP commitment to climate investing will be, particularly in the US, as the Trump administration loosens environmental impact standards, limits or freezes the flow of government funding to companies in this space, and makes it more difficult to complete projects, most recently via the One Big Beautiful Bill Act. While fundraising data through Q1 likely does not yet reflect many of the year's policy developments given the time it takes funds to close, there is reason for optimism around the space's future, with technological maturity; structural demand for affordable energy, energy security, and secure food systems; shifting consumer preferences; and other tailwinds. Read more on this topic in our free research: Climate PE Funds: Heating up or Cooling Down? Clients can access the full version of this and other LP-focused commentaries in our dedicated workspace. | | Best,

Anikka Villegas

Senior Analyst, Fund Strategies &

Sustainable Investing | | | | | | | | | |

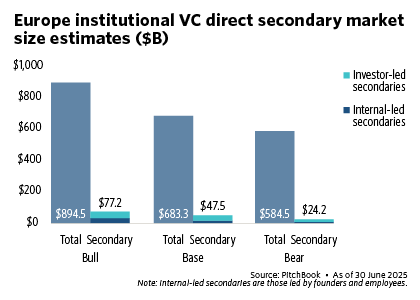

Sizing the Institutional VC Direct Secondaries Market

Institutional VC direct secondaries are emerging as a dynamic segment of the private markets, with global deal value reaching $14.7 billion in 2024—the highest annual figure since 2021.

Our analyst note spotlights the evolving role of secondaries, where nearly $113 billion of institutional VC direct secondaries has been transacted globally since 2015. | |

As secondary deals become a more prominent exit route, especially in liquidity-constrained environments, this trend could reshape exit strategies across early- and late-stage VC portfolios.

Read the free research | | | | | | | | | |

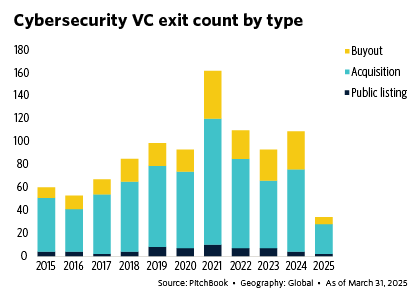

Cybersecurity VC Trends

Cybersecurity startups raised $3.3 billion across 182 deals in the first quarter of 2025, flat in value from the prior quarter with a drop in deal count. Consolidation emerged as a defining theme, with larger firms acquiring specialized capabilities to strengthen platform breadth and close product gaps. | |

Segment activity remained concentrated in security operations, identity and access management, and application security. With US federal cybersecurity funding at record levels and late-stage valuations recovering, the sector is being shaped by structural drivers favoring platform-oriented scale.

Read a free preview

| | | | | |

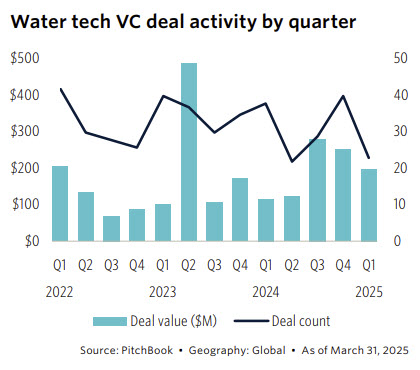

Water Tech

VC activity in the water tech sector remained resilient in Q1, putting this year on track to match the strong total from 2023 and 2024.

The sector is attracting significant investment in areas like water treatment, desalination, and mineral extraction from water sources.

| |

Despite policy headwinds and cost challenges in some regions, our new research explains why water tech is increasingly seen as a critical enabler of climate resilience, infrastructure continuity, and resource independence:

Read the free research

| | | | | | | | | |

July 31: Halfway through 2025, the venture market remains defined by liquidity concerns and surging interest in AI. Our experts will examine current US VC trends, analyze their impact on the market moving forward, and offer their outlooks for the rest of the year. More information here.

Sept. 18: Our senior analyst Anikka Villegas will be presenting at Morningstar's Sustainable Investment Summit, covering the future of climate, ESG, and DEI in private markets. Register today to gain insights on investor trends, performance, and diversity. | | | | | | | | | |  | | Senior analyst Emily Zheng talks VC IPOs and more. | | |

Our insights and data featured in the press:

• Discussing VC trends in the first half of 2025. [Bloomberg Technology]

• Venture capital investment in climate tech fell in 2024 for the third consecutive year. A report from PitchBook suggests those investments could fall even further in 2025. [Fast Company]

• So far this year, the amount raised by US PE-backed listings is up 75% from all of 2024—the biggest jump since 2021. [Bloomberg]

• Robotics companies, which have received around $3.5 billion in investment since 2019, are making food delivery better, faster and cheaper. [The Wall Street Journal]

• With European VC funding down, startups are leaning more heavily on angel investors. [Sifted] | | | | | | | | | | | | | | | | | | | | | | Since yesterday, the PitchBook Platform added: | | 611 Deals | 2472 People | 804 Companies | 13 Funds | | | | | | | | | | | | | | |

No comments:

Post a Comment