| | | Healthcare funds: Healthcare-focused GPs are standing out in a tough fundraising environment. Our new report looks at 512 healthcare and life sciences specialist managers across PE and VC, highlighting their activity and performance. Read more.

APAC IPO opportunities: APAC's IPO markets are entering a new era—one that is narrower and more selective but far from closed. Our research note examines this evolution. Read it here.

Popular research: In case you missed them, here are three of our most-read notes over the past few weeks:

• The Evolution of Biotech Funds

• US VC Secondary Market Watch

• Private Capital in Sports: PE Is Up to Bat | | | | | | | | | A message from AlixPartners | | | | AI Playbook for PE Operating Partners: From readiness to results | | AI's potential is real, but without effective execution, even the best strategy stalls. For Operating Partners, the ability to drive alignment, ensure adoption, and scale proven models across portcos is where value is truly created. A well-executed AI initiative can accelerate EBITDA expansion, strengthen leadership buy-in and create measurable, repeatable results across the portfolio.

The third step in turning strategy into scalable value focuses on what it takes to move from planning to action. From clearing organizational roadblocks to embedding performance metrics and sustaining momentum through change management, explore how OPs can lead transformation that lasts. Read the playbook for operating partners here | | | | | | | | | | | Why PE is at a crossroads with transportation and logistics | | The transportation and logistics industry is evolving rapidly, driven by shifting global trade patterns, technology, heightened customer expectations, and climate concerns. Geopolitical tensions, regional disruptions, and post-pandemic reevaluations of risk are forcing diversification and a shift from just-in-time to just-in-case frameworks for supply chain planning and deployment. The structural changes are prompting a shift toward more agile, responsive, and technology-integrated logistics systems, according to our debut Transportation & Logistics Report.  | | Clients get access to the full market map. | New technologies continue to reshape the industry with the adoption of AI, the internet of things, digital freight platforms, and autonomous systems. Real-time visibility, predictive analytics, and warehouse automation are becoming necessities to meet ever-higher customer expectations for speedy deliveries and tracking. Decarbonization and sustainability are key drivers of change as the movement of goods around the planet by ship, rail, and truck has an outsized impact on climate change. Regulatory pressure and investor scrutiny are pushing logistics firms to cut emissions, reduce waste, and adopt greener tech. Warmer global temperatures are opening new and significantly shorter trade lanes in Arctic regions, prompting a reevaluation of trade routes and technologies for operating in those areas. Additionally, the industry faces trade and tariff uncertainty, labor shortages, high fuel costs, and infrastructure bottlenecks, which stymie efforts to maintain profitability and service levels. Long-term success depends on adaptability, agility, and strategic investment in this environment of disruption and rapid innovation. PE deal activity in the sector peaked in 2021 and declined through 2024. In Q1, however, the run rate appears to be lifting due to greater investor interest and scrutiny of supply chain activity and challenges. For a deeper dive into industry trends and dealmaking activity, read a preview of our Transportation & Logistics Launch Report, as we introduce new full-time analyst coverage of the industry. | | | | | | | | | The secondaries renaissance | | Secondaries funds raised a record amount of capital in 2024, topping the 2020 record by $10 billion. Through Q1, the strategy is already on another record pace, coming in at just under half of the capital raised all of last year. In a period when fundraising has been incredibly difficult for other strategies, particularly VC and real estate, it has been unusual to see records being set anywhere.  | | | What has been driving this interest? First off, the secondaries universe isn't particularly expansive. The fund families that fed the 2020 record exhausted their commitments after a few years and came back to market, leading to a predictable wave that started in 2023 and continued into 2025. In January, Ardian Secondary Fund IX raised $30 billion, much more than its $19 billion predecessor that closed in 2020. Second, the rise of GP-led secondaries has expanded the size of the investable market and attracted GPs to the space. Apollo, Brookfield, Accel-KKR, and TPG have all launched secondaries funds larger than $1 billion since the start of 2024. Third, some LPs have taken an "if you can't beat 'em, join 'em" approach to GP-led secondaries. LPs who cash out when a continuation fund is on offer—either because they want to or because their governance structure will not allow them to roll into a continuation fund—may be missing out on the upside at exit that the new GP entrants see as likely, so investing in secondaries funds could replace that source of value. Another new factor that could lead to secondaries deal flow is proposed legislation that could result in the largest endowments facing potential tax rates up to 15x what they have paid previously—and some may be considering the sale of illiquid investments to free up cash to pay their tax bills. For more data and analysis on secondaries and other strategies, download our Global Private Market Fundraising Report. Clients can access the full version of this and other LP-focused commentaries in our dedicated workspace. | | | | | | | | | | | |

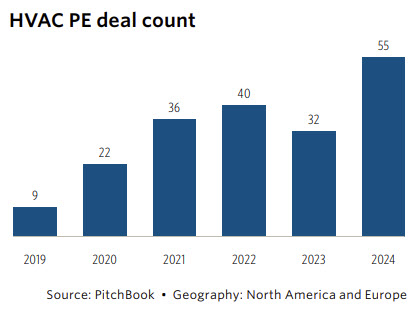

Clearing the Air on HVAC

PE interest in the HVAC sector remains robust, with a record 55 deals in 2024—a 72% increase year over year.

| |

This surge is driven by the industry's essential role in infrastructure, its fragmented nature, and the increasing demand for energy-efficient and tech-enabled solutions.

Despite challenges such as tariffs and supply chain disruptions, the sector's resilience and growth potential continue to attract investors:

Preview our premium research

| | | | | |

Enterprise SaaS M&A Review

The enterprise SaaS sector has experienced a notable resurgence in M&A activity.

This recovery signals renewed confidence from PE firms, even as strategic acquirers have refrained from large deals amid persistent economic uncertainty and greater regulatory scrutiny.

Despite this recovery in volume, the overall value of SaaS M&A dropped by nearly 25% QoQ as the market continues to grapple with valuation pressures:

Read the free research

| | | | | | | | | |

2025 Midyear Outlooks Webinar Series

July 8-23: Join this webinar series to explore shifts in private market expectations halfway through 2025, amid increased uncertainty across the VC, PE, and credit segments. We'll also have regional sessions for EMEA and APAC. More information here. | | | | | | | | | |

Our insights and data featured in the press:

• PE firms have had difficulty returning cash to investors at levels reached in previous years. [NYT]

• Investors have poured more than $150 billion into defense startups since 2021. [FT]

• Why secondaries funds are booming. [P&I]

If you're a journalist interested in interviewing our analysts or requesting data, contact our PR team.

| | | | | | | | | | | | | | | | | | | | | | Since yesterday, the PitchBook Platform added: | | 594 Deals | 2099 People | 825 Companies | 38 Funds | | | | | | | | | | | | | | |

No comments:

Post a Comment